No items in the cart

Expatriation: what health insurance have we chosen?

Among the most expensive expenses for an expatriation,expatriation health insurance is at the top of the list along with school fees.

In this article, we will share with you our PERSONAL experience and hope that the information will be useful for your (future) expatriation, whether it be to Malaysia or another country.

For

living in Malaysia

You must evaluate your budget in order to avoid unpleasant surprises once you arrive in Malaysia.

In this article, we will expose our small guide to choose your health insurance, starting by giving some examples of prices for care in Malaysia, the criteria to take into account to make your choice, the different insurance solutions in Malaysia, the insurance companies we compared, our choice in 2020 and 2021, and finally, some concrete examples of care done in Turkey in 2020 and Malaysia 2020 and 2021

In addition, all this will be illustrated through a video available on our Youtube channel.

Disclaimer

Everything described in this article is based on our own personal experience, unless otherwise stated.

We are not specialists in expatriate insurance. If you have any questions regarding services, you should contact these professionals directly.

There are no affiliation links in this article: all the names of the professionals listed below are for information purposes only.

We do not receive any remuneration for quoting these companies.

We just hope that this article could help some people or families in their expatriation project.

Outline of the article

I – Example of health costs in Malaysia

1) Fees in public hospitals

2) Fees in private hospitals

3) Example with the hospital in Kuala Lumpur

4) What are the differences between public and private hospitals?

5) Which health insurance should I choose?

6) Why take out health insurance?

II – The different forms of insurance in Malaysia

1) Malaysian local social security

2) Foreign Workers Hospitalization & Surgical Scheme (FWHS or SKHPPA)

3) Takaful Insurance

4) Malaysian local insurance: only for unforeseen health expenses

5) International insurance: for customized global coverage

6) Travel insurance

III – What type of insurance have we chosen?

1) Local or international insurance?

2) The different types of international insurance: CFE / CFE + complement / 1st euro insurance

IV – What criteria should I take into account when choosing my insurance?

V – International insurance companies: compare quotes and choose

VI – How much does the chosen insurance cost?

1) CFE + Malakoff Mederic, in 2020 and 2021

2) Our health insurance for 2022: MSH International ?

3) What insurance for the following years?

VII – Example of expenses in Turkey

VIII – Example of fees in Malaysia

1) Dental expenses

2) Vaccine costs

3) Optical expenses

IX – Our advice

I – Example of health costs in Malaysia

I will give you some examples of prices, so that you can understand the different issues, before deciding anything.

The prices below are taken from various websites.

Please note that these are only average prices for information purposes!

The average cost of healthcare in Malaysia is much lower than in Europe, and also much lower than its neighboring country Singapore, or the United Arab Emirates (Dubai, Abu-Dhabi, etc.) which remain a preferred destination for many expatriates, especially online entrepreneurs.

Note that the fees are different for Malaysian citizens (including those with permanent residence cards) and foreigners: when you look at the fees, make sure they are for foreigners and not for Malaysian citizens.

Foreigners will pay more than Malaysian citizens.

In the last chapter of this article, we will give the costs of the different treatments we had to pay in Turkey (between June and November 2020) and in Malaysia (since November 2020).

1) Fees in public hospitals

Consultation of a general practitioner in a public hospital or clinic: RM20-25 (€4-5)

Specialist consultation in a public hospital or clinic: RM 120-150 (€25-30)

Hospital admission fee: RM 15-35

Stroke treatment: RM4000 (€800)

Kidney stones: 3000 to 10000 RM (depending on the complexity – 600 € to 2000 €)

Rooms: RM 3 to RM 80 per day (depending on the type of room – 0.90€ to 1.6€)

Radio : 10 RM (2€)

Ultrasound: 10 RM to 100 RM (2€ to 20€)

Blood test: 1 RM

General anesthesia: free (depending on the situation)

2) Fees in private hospitals

Consultation of a general practitioner/specialist in a private hospital: RM 30-250 (€ 6-50)

Hospital admission fee: RM 500-2000 (€100-400) or as a percentage of hospital care.

Stroke treatment: RM35,000 to RM75,000 (€800 to €1500)

Kidney stones: RM 9000 to 40000 (depending on the complexity – € 1800 to € 8000)

Rooms: RM 80 to RM 300 per day (depending on the type of room – €16 to €60)

Radio : 35 RM (7€)

Ultrasound: RM100 to RM300 (€20 to €60)

Blood test: RM 50 (€ 10)

General anesthesia: RM 1000 (€ 200)

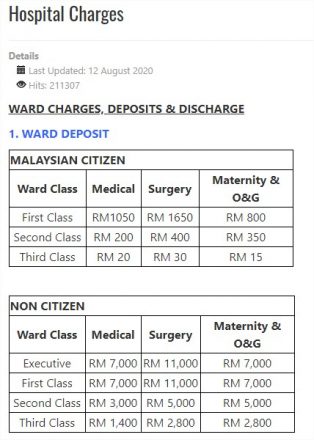

3) Example with the hospital in Kuala Lumpur

You can also consult the rates directly on the hospitals’ websites.

Example below, with the Kuala Lumpur Hospital (HKL):

4) What are the differences between public and private hospitals?

Private hospitals are more expensive than public hospitals.

They offer better services, but this does not mean that they will provide better care than public hospitals, which are also well known.

This will be differentiated in terms of time to care, ancillary services, choice of doctors, maintenance and cleanliness of the hospital environment, as well as other amenities (meals, refrigerator, space, television, etc.).

Generally, private establishments also avoid the long waiting lines of public hospitals (which can be very long…).

Public hospitals are called “general hospital” or “hospital umum”.

Public clinics are called “Polyclinics” or “Poliklinik”.

5) Which health insurance should I choose?

So you have several choices regarding your health insurance:

- You decide not to take it, considering that you are in good health and would rather pay out of pocket when care is needed. I don’t recommend this choice because accidents never happen (car accident, serious illness, etc.). You will have to pay all the costs out of your own pocket. We will no longer talk about 50€ or 200€ but the bill can very quickly reach 5 or 6 figures…

- You decide to take out insurance that covers everything, i.e. hospitalization (accidents, etc.) as well as routine medical care (consultations, medication, X-rays, etc.) for the whole family (or just you if you are alone).

- You decide to take out insurance that covers the biggest unforeseeable expenses (hospitalizations/accidents), and you customize it according to your personal needs (routine medical, optical, dental, and maternity). And you will pay the difference out of your own pocket, to supplement the costs, if necessary.

6) Why take out health insurance?

Simply to protect you in case of accidents, including emergencies, unforeseen hospitalization costs, accidents, etc.

Insurance also allows you to live your expatriation with peace of mind, which is even more important when it is a family expatriation.

Some people, under the pretext that they are in good health, do not take out any insurance, for budgetary reasons: for our part, we absolutely did not want to do without our health coverage.

II – The different forms of insurance in Malaysia

The different solutions to be covered in Malaysia:

1) Malaysian local social security

This is called PERKESO (Pertubuhan Keselamatan Social) or SOCSO (SOcial SeCurity Organization).

As in France and other countries, PERKESO aims to help people without resources (unemployed, sick, or deceased).

Both the employer and the employee contribute to this.

Since January 2019, foreign employees are compulsorily contributing to this fee (RM49.40 per month).

More information on the official website.

It will only cover accidents in your workplace.

Normally, you do not have to pay this contribution if you are self-employed, have your own company, or work for the government.

It is an insurance that covers until the age of 55.

It does not cover your family.

And people who are self-employed are not covered.

In short, it’s not for us.

2) Foreign Workers Hospitalization & Surgical Scheme (FWHS or SKHPPA)

This is an insurance for all foreign employees.

You will not have a choice of hospital: it is limited to government (public) hospitals.

For RM120 (€24) per year, this insurance will cover you up to RM10,000 (€5,000).

This includes:

- Hospital and room charges for up to 30 days per year,

- Intensive Car Unit (ICU) for up to 15 days,

- Operating costs,

- Surgical and anaesthesia expenses,

- Specialist consultations during your hospitalization, up to 30 days,

- Ambulance fees,

- Medical reports.

This is not the right solution for a family.

3) Takaful Insurance

It is an insurance based on Islamic laws.

It is an insurance that aims to avoid prohibitions such as Riba / interest etc.

It differs from traditional insurance in the way it works.

It is not exclusively reserved for Muslims.

Personally, we do not have enough experience to give our opinion on this solution.

4) Malaysian local insurance: only for unforeseen health expenses

There are severallocal insurance companies.

They usually offer a plan for your life, health and retirement insurance.

Generally, you will only be covered in the insurance’s hospital network, and you will not have to pay anything in advance (tiers-payant).

If it’s out of network, you’ll need to contact your insurer beforehand to check the conditions etc. Medical expenses: normally, you should be covered but you should advance the expenses, then send the bills to the insurance company to claim the reimbursement.

You can buy this contract through agents who are there to advise you as best as possible (and who earn their commissions).

You have for example the following insurance companies, which are the most widespread in Malaysia:

We made some estimates with these insurers, but for the moment, that does not suit us compared to our criteria (covers, expenses, etc.).

You also have other local insurance companies such as:

Great Eastern Life

Hong Leong Insurance

AXA

Each company has its own system, with its own advantages and disadvantages.

AIA, for example, is the only one to date that covers the cost of mental disorders.

With Prudential, you can choose the coverage you want, but, as with other local insurances, it will not cover routine health or maternity expenses.

5) International insurance: for customized global coverage

This is the one we chose because it best suits our needs.

We keep in mind the local insurance, and depending on the evolution of our life in Malaysia, we will see if we will switch to a local insurance or not.

For the time being, we will not take any risk and we prefer to keep more or less the same coverage as we had in France.

The international insurance covers us in Malaysia, but also in other countries, notably France, Morocco, or Cambodia, where we would often go: in short, as its name indicates, this insurance covers you everywhere in the world (check the different conditions with each insurer).

Moreover, with the COVID-19, it would not be wise to take risks to save a few euros per month.

The quotes are made from companies in France, and therefore, in French language.

In French, the conditions and details are not always easy to understand, so if you turn to a company that gives you a contract in English or in another language (unless you are bilingual), it could be even more complicated!

It is this type of insurance that we will detail in this article.

6) Travel insurance

This is an insurance that you can take from the same local insurance companies.

It is important to know that local insurances only cover you locally.

Therefore, when you travel, you will not be covered.

However, the solution would be to take out travel insurance during your stay abroad.

Some people opt for this kind of insurance from France, considering that they will be traveling in Malaysia.

This is not a solution that suited us because Malaysia is our main country of residence.

It is a solution rather intended for a short stay in Malaysia. In addition, this type of insurance does not usually cover everything.

Finally, for international students, there is an insurance that is Education Malaysia Global Services (EMGS).

You should contact your school, if this concerns you.

You will find on this site, many information for students.

III – What type of insurance have we chosen?

1) Local or international insurance?

For the first year, after having studied the different possible solutions, we chose an international insurance, as a precaution.

Indeed, this insurance covers the whole family, whether in Malaysia, France or elsewhere in the world.

Over time, we will make the necessary optimizations based on our annual health care expenses.

Eventually, we should opt for a local insurance (classic or takaful, it is still to be determined), and a travel insurance in case of travel.

2) The different types of international insurance: CFE / CFE + complement / 1st euro insurance

CFE only

The CFE is the Caisse des Français à l’Étranger.

It aims to offer the same social protection as in France.

Who can subscribe?

French nationals, EU, EEA (European Economic Area) and Swiss nationals, regardless of your family situation, professional status, country of residence, age or health status.

The CFE allows you to benefit from guarantees similar to those of the French Social Security.

You will find all the information you need on their website, including the fee schedule, as well as details about the coverage and the various benefits.

One of the advantages of the CFE is that it allows you to benefit from your rights when you return to France, without any waiting period.

If after one year of expatriation, we have to return to France, we will be able to reintegrate our social regime immediately.

Just like in France, social security is not enough to cover all health expenses.

This is why there are mutual insurance companies that will allow you to complete your basic social coverage.

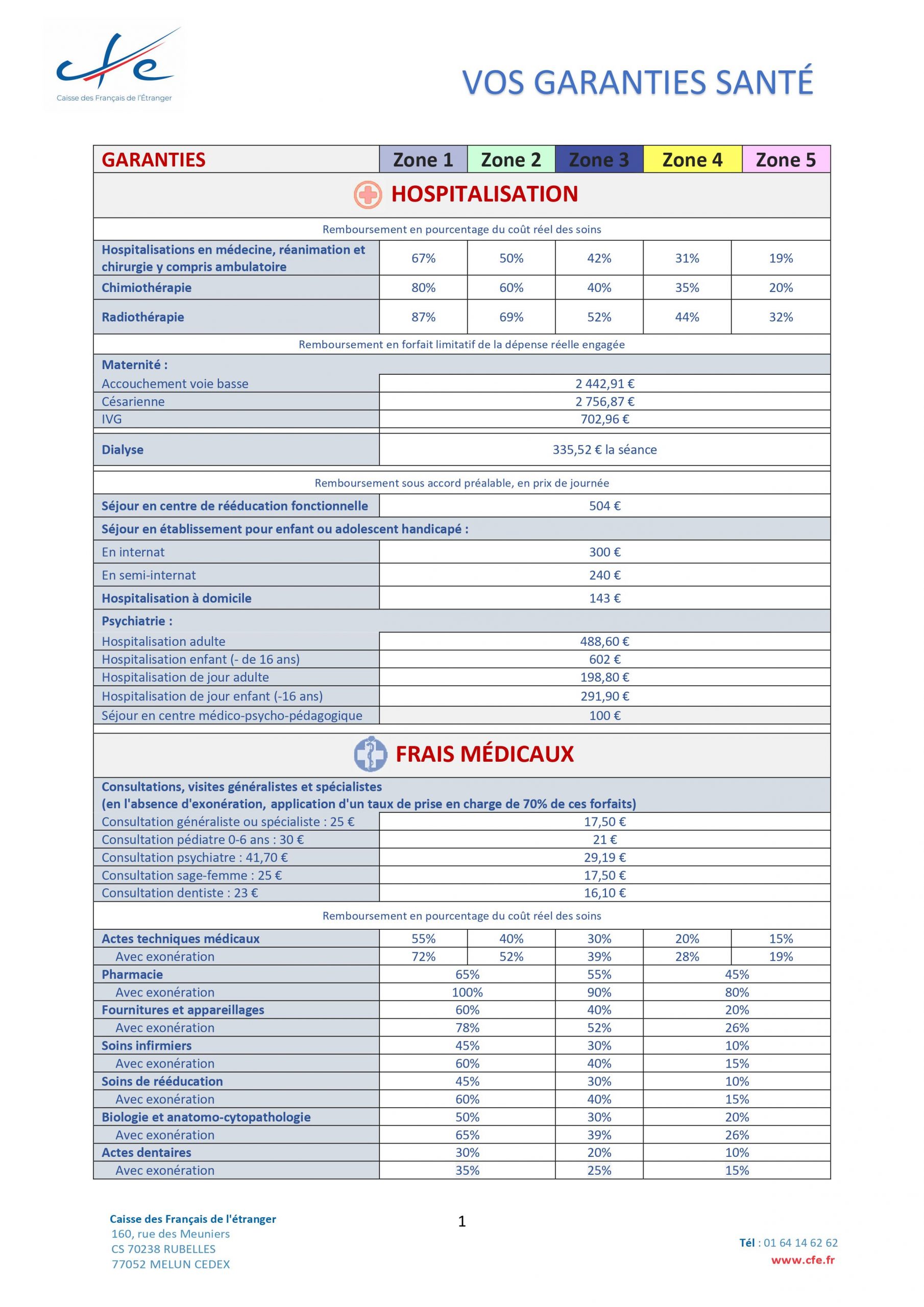

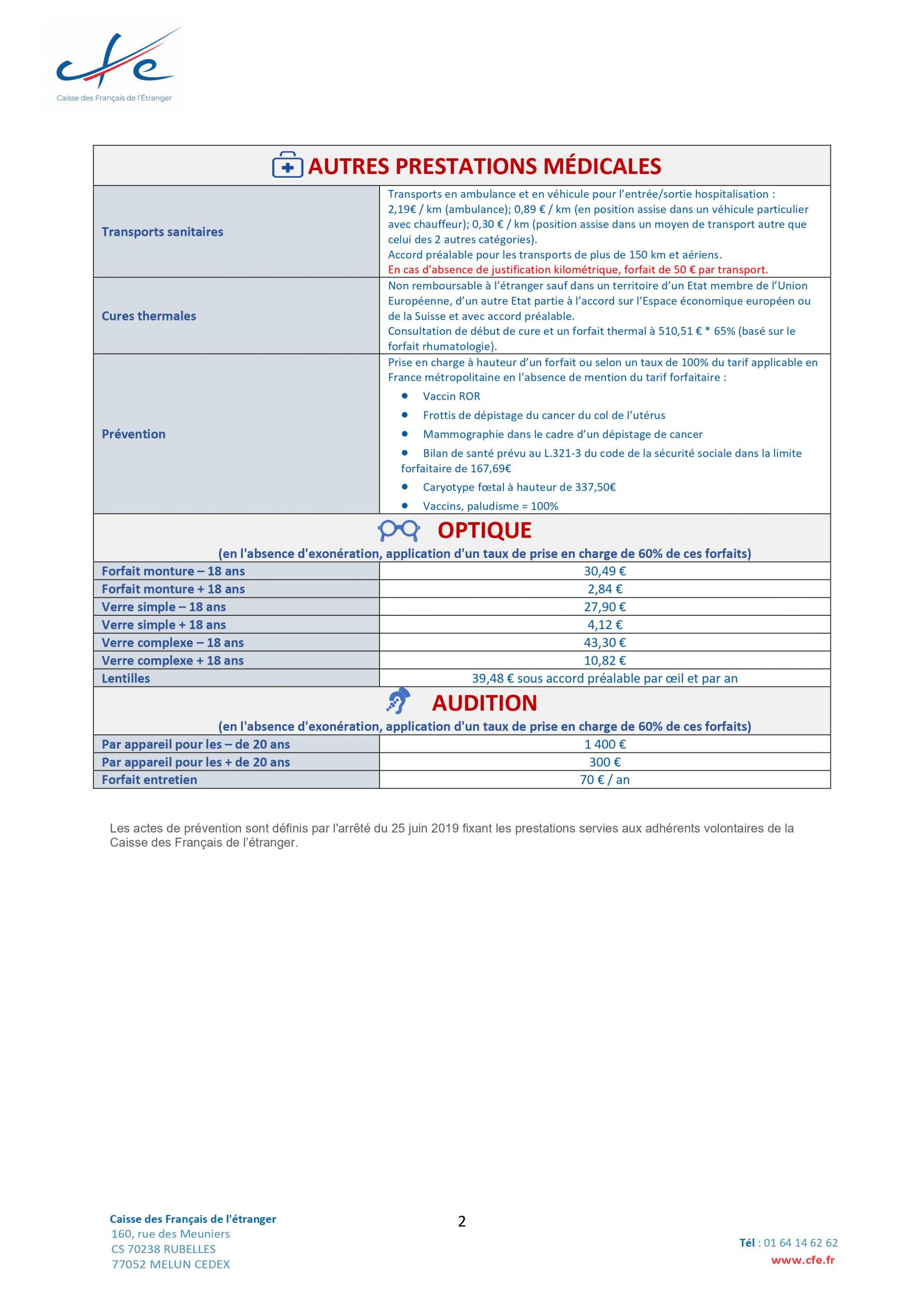

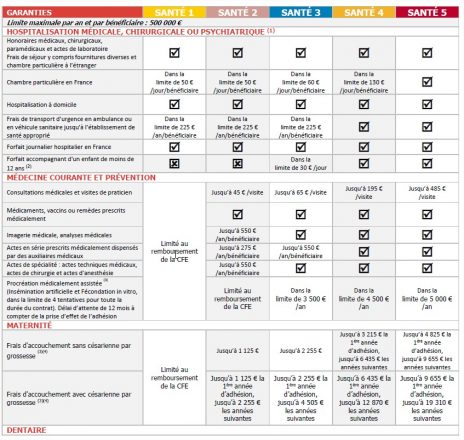

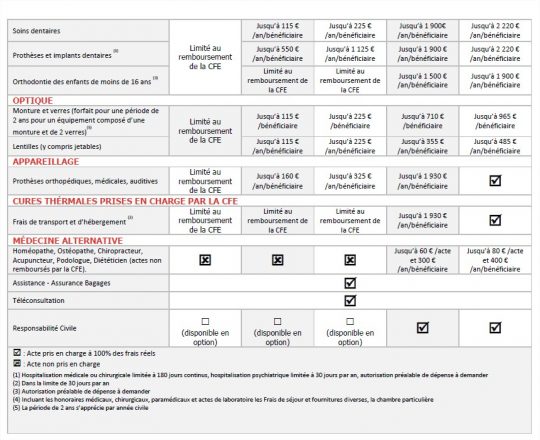

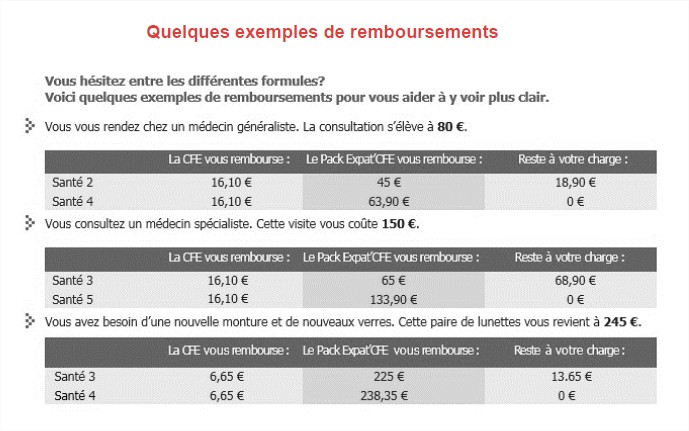

Here is the table of benefits for 2021:

CFE 2021 HEALTH BENEFITS

CFE + complementary mutual insurance

For better health coverage, you can opt for a complementary CFE.

This is what we have chosen for the first 2 years.

However, there are a multitude of insurers.

It is thus necessary to compare well, and to make the good choice:

- Do not underestimate your needs,

- Do not overestimate your needs.

The difficulty lies at this level: how to make a good estimate of the costs of health care in the country of expatriation?

We will detail our choice in the following section.

Insurance at the 1st euro

You sign up with one organization.

The latter will be the sole interlocutor.

What is the difference with CFE + complementary health insurance?

Unlike the CFE + complementary solution, this insurer will take care of the reimbursement of your health care, from the first euro.

The guarantees can also be different with the CFE + complementary solution, so it is important to study your personal needs.

The price is also different: according to our quotes, this solution is generally more expensive. The conditions to subscribe are also different.

CFE also offers professional risk insurance and a pension.

IV – What criteria should I take into account when choosing my insurance?

Before making our choice, several criteria come into play.

On the basis of the few criteria below, we have progressively made our choice, by elimination.

Among the criteria to consider, you have:

- Age: some insurance companies will not offer you insurance after a certain age. It can be 70 years or 50 years etc.

- Your current physical condition: if you are undergoing a particular treatment, you will have to check this in the contract of your insurer.

- Your lifestyle: if you travel often, or if you engage in riskier activities, etc. A sedentary person and a regular traveler will not have the same needs.

- Your budget: prices vary greatly between different insurers. We need to multiply the quotes.

- Coverage limits: you can make your own estimate based on your health needs

- Franchising: with or without a franchise?

- Geographic coverage: do you want coverage only in your country of expatriation or worldwide coverage?

- Non-covered care: some insurances offer additional options such as assistance and medical repatriation, others include them in their basic formula, etc.

- How it works: how to get reimbursed, third-party payment, the global network, etc.

- The different formulas offered: some companies will only offer insurance from the 1st euro, others only the CFE + supplement, etc.

- The contract: check the flexibility, the length of the commitment, the possibility of changing options during the year, the waiting period, the cancellation conditions, etc.

- Quality of service: are they responsive? Do they speak French? Is their website easy to use? etc.

V – International insurance companies: compare quotes and choose

We have selected several insurance companies.

There are dozens and dozens of them, knowing that nothing obliges you to take a French insurance.

I prefer to warn you that choosing insurance takes time: time to determine your precise needs, time to receive the different quotes, and finally, time for reflection and the final decision.

Here are the different insurers we compared on our side (again, this is an article without any affiliation, and based only on our personal experience) :

- April International: instant online quote

- Henner

- Malakoff Humanis: quotes generally received in less than 48 hours

- MSH International: instant online quote

- Allianz Travel

To make our choice, we created an Excel file, gathering all the important data in our eyes, and then, with a clear head, we made our choice.

The first and second year, we finally chose to leave for CFE + MALAKOFF HUMANIS.

The following year, we should move to MSH International, with a franchise.

Then, as said before, we will probably switch to a local insurance, depending on the evolution of our situation in Malaysia.

VI – How much does the chosen insurance cost?

1) CFE + Malakoff Humanis, in 2020 and 2021

We therefore chose CFE + Malakoff Humanis, with formula 1.

The CFE contribution (Mond’Expat CFE, sickness and maternity) is 2112 € per year, for the whole family.

The Malakoff complementary contribution amounts to 1331 € per year, for the whole family, without deductible.

Here are the details of the HEALTH 1 benefits.

That is to say a total of 3443 € per year, or 287 € per month.

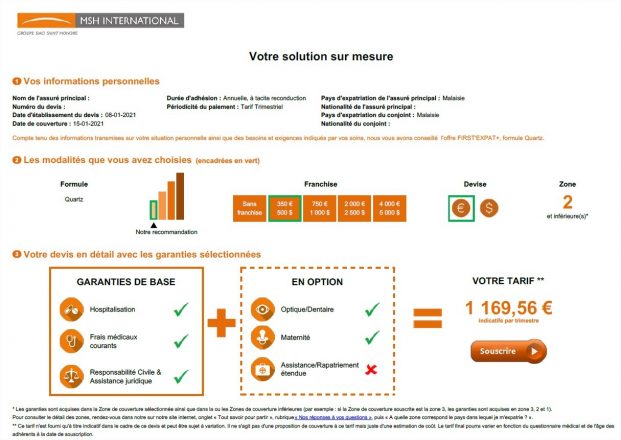

2) Our health insurance for 2022: MSH International ?

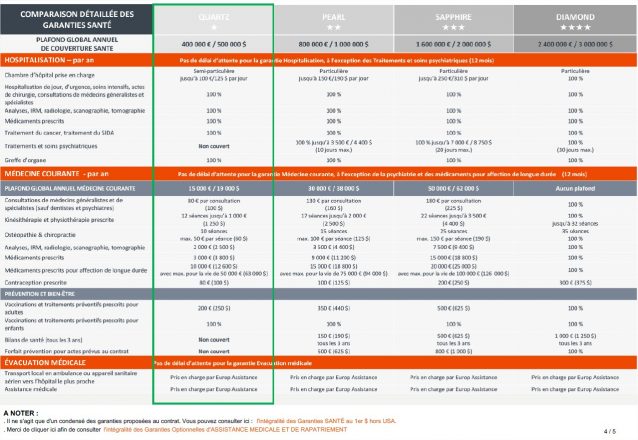

For 2022, we will probably switch to MSH International, Quartz formula, with a deductible of 350€ per person, but a total coverage on current health expenses.

The annual fee would be 4680 €, or 390 € per month for the whole family.

However, we will also be insured on the optical and dental part.

Again, it is important to calculate your personal needs.

The monthly fee is higher, but in the end, with the dental and optical fees and all the different consultations (pediatricians, general practitioners, and other specialists), it may be cheaper than the current formula.

Above all, it will also give us a psychological comfort, to say that everything should be covered, in case of glitches.

The decision has not yet been made, we will make an assessment at the end of 2021.

But this other quote might give you a little more idea of what to budget for health insurance.

3) What insurance for the following years?

We are thinking of switching to a local insurance company, and paying out of our own pockets for all our current health expenses: consultations, dental and optical care, vaccines, medication, etc.

This insurance will therefore only cover unforeseen medical expenses (not routine health expenses).

With a local insurer, we would complete with a travel insurance when necessary (trip to France or vacations etc.).

With our first quotes at PRUDENTIAL, here is the average budget to expect, again, based on our own personal needs (so the price can go down or up considerably depending on your situation) :

For both parents: 100€ to 180€ per month

For 1 child: 47€ to 82€ per month.

In total, for a couple with 1 child, this would be around 135€ to 195€ per month.

VII – Example of expenses in Turkey

All of the following treatments have been reimbursed by CFE, as we have no coverage for routine health care (consultations, X-rays, blood tests, etc.)

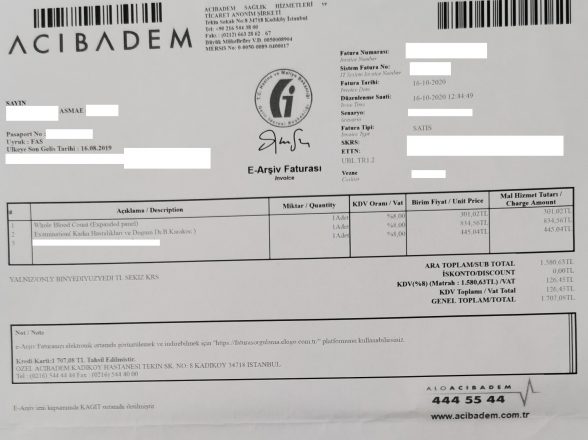

Below is an invoice for 1708 TL.

This represented at the time approximately 186 €.

We were reimbursed 45.80 €, or about 25%.

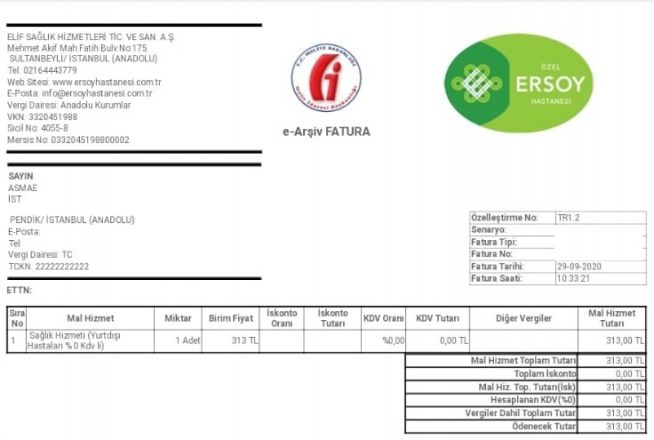

The invoice below is 313 TL, and we have been reimbursed 30% of the amount

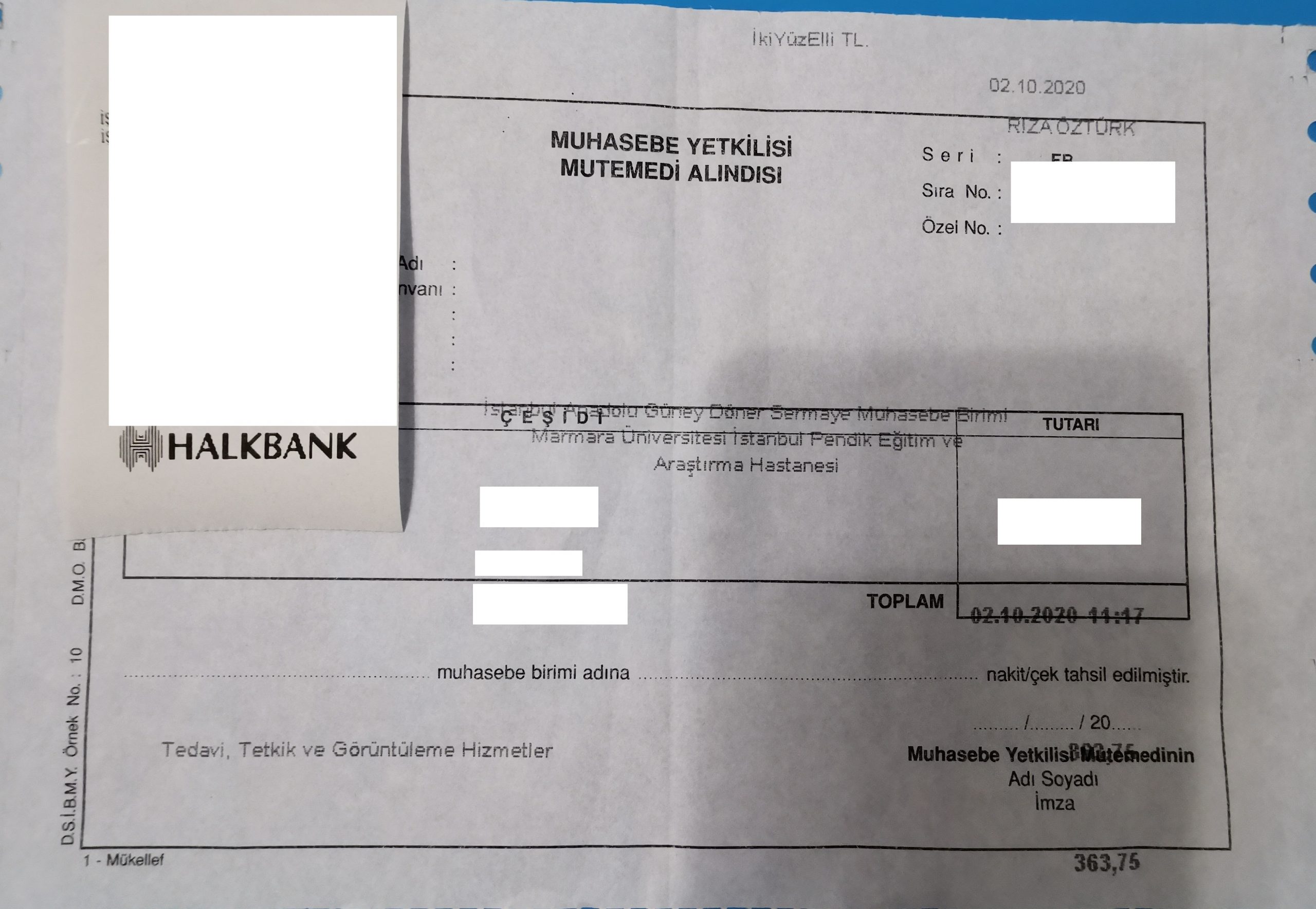

Finally, another bill, this time in a public university hospital (which we do not recommend at all!).

We were reimbursed 50%.

VIII – Example of fees in Malaysia

Here are some concrete examples of some of the treatments performed in Malaysia.

This will give you a clearer idea of the health budget for Malaysia.

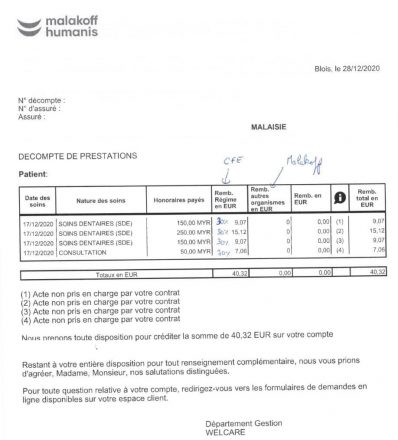

1) Dental expenses

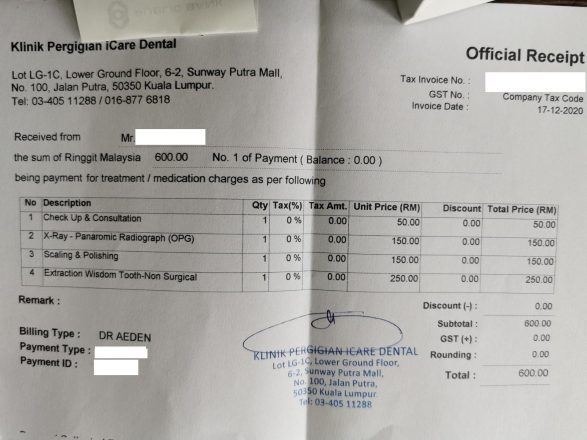

Due to dental pain, I had to see a dentist, have an X-ray, and extract a wisdom tooth, as well as a scaling.

Here are the details of these treatments, below:

Likewise, only CFE reimbursed the expenses up to 30% for dental care, and 70% for the consultation.

Here are the details of the refunds:

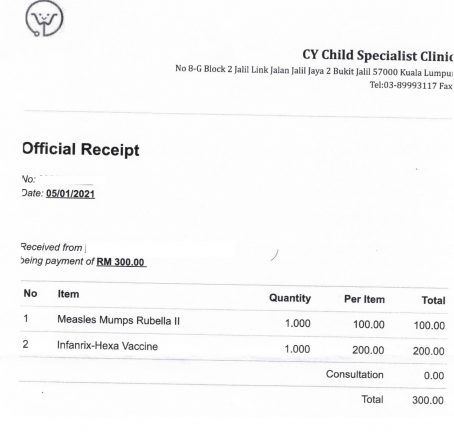

2) Vaccine costs

Of these costs, CFE reimbursed about 66% (within 2-3 weeks).

3) Optical expenses

For branded frames, with corrective lenses, I got them for :

- Hugo Boss frame (solar without lenses)

- Prada frame + lenses

1651 RM, or about 335 € for the 2 frames including 1 with corrective lenses.

I have added RM 250 for sunglasses.

That is to say approximately 385 € for 2 pairs of branded glasses, with correction.

No reimbursement from the CFE because I haven’t done the necessary steps yet: normally, they take care of 2.84€ for the frames, and 4.12€ for the lenses.

The reimbursement is therefore very low on this part.

For frames + lenses of local brand(Woosh), Asmae got them for 70 € (you have cheaper too).

You can find corrective eyeglasses much cheaper as well.

4) COVID and other tests

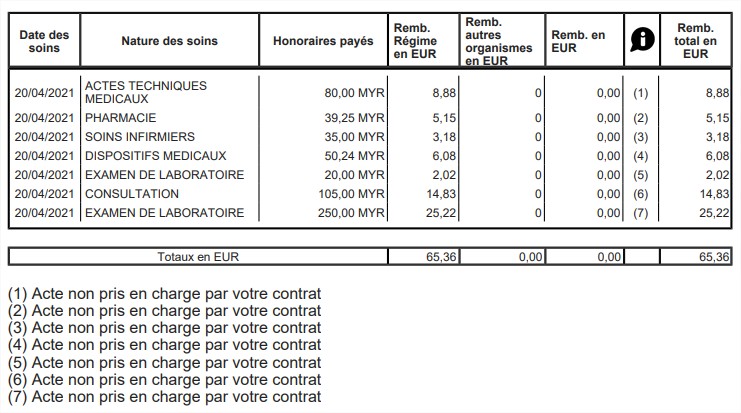

Recently, in April 2021, we had to do a COVID test (SWAB PCR TEST) here in Malaysia.

There were also other medical procedures.

Here are the details of these benefits:

IX – Our advice

- Don’t wait until you’re sick to get insurance.

- Take the time to make the comparisons.

- If you are moving abroad, the first year it is better to start with a slightly higher coverage than you expect, then optimize over time.

- The emergency number in Malaysia is 999: keep it in mind in case of need (police, firemen, etc.).

- Also, keep the contact information for the embassy in your home country in case of need.